12 Bad Business Ideas the Data Killed in 2026

Key Takeaways

Most bad business ideas do not look bad on paper. They look endorsed, funded, and trending, which is what makes validating an idea before you build so hard. A founder publishing on Indie Hackers in February captured the pattern we kept seeing in May 2026:

“I spent weeks writing a 50-page PRD, a 24-task execution plan, and a 14-day promotion playbook, then watched a landing page sit completely empty. This is the postmortem I wish I'd read before I started.”

Five days. Zero signups. One channel. The category had named adjacent funded competitors. The math looked clean on paper. But the buyer-search velocity, when anyone bothered to check, was absent.

That same pattern repeated across more than 4,000 ideas we tracked in May 2026.

Here is how the report came together. Fluenta monitors a standing registry of more than 180 authoritative sources, accelerators, venture funds, consulting firms, global business media, and 130-plus regional outlets across 13 regions. In May 2026, 74 of them actually produced ideas worth logging. Product Hunt dominated the volume, north of a thousand submissions on its own. YC came next, then a16z close behind. The consulting firms (McKinsey, BCG, PwC) and the tech press (TechCrunch, CB Insights, Forbes, Reuters) filled the middle, with GitHub Trending tracking developer momentum. A long tail of accelerators, niche newsletters, and regional VCs (Stanford Blockchain Accelerator, Draper Associates, Latitud, and 60-plus others) made up the rest.

After deduping May's haul by title, 4,018 ideas were unique, and only six appeared in two or more sources that month. But exact titles undercount it. Match our scored ideas by meaning instead of wording and about one in fourteen turns out to be the same concept reworded, 43 clusters in all. Most of that repetition is one source echoing itself; only eleven clusters span more than one source. So "everywhere this week" in 2026 is mostly a single loud source repeated, not many independent sources converging.

From those 4,018 we pulled 393 for full scoring across 16 collections, including a set that rolled over from the April 29 batch. We published 25 of the scored ideas on the May Saturday Kill Lists, one batch a weekend. Twelve came in under 32 on the Launch Readiness Score (LRS). The floor was 23.4.

What killed them was not opinion. Each idea ran against six independent signals, everything from buyer-search demand to funding momentum to whether anything actually made the decision urgent. The numbers came back weak in the same way across almost all of them. Median search volume across the twelve was 50 a month, and most showed no real buyer intent at all. Nine had seen no category funding in 18 months, headlines notwithstanding.

So here is the list: the 12 names, the score each earned, what the six signals showed, and why it matters whether you write about these categories, fund them, or build in them. The gap between "described by McKinsey" and "searched on Google" runs about 12 months, and it shows up on no portfolio dashboard anywhere.

Source · Fluenta, May 2026

How the report came together

Before scoring, ideas have to be scouted. Fluenta monitors a standing registry of more than 180 authoritative sources across 13 regions, and in May 2026, 74 of them produced ideas worth logging. These are the same sources VCs, journalists, and operators read every week. We do not generate ideas ourselves. We observe what the public ecosystem flags as worth attention.

The volume splits into six source types. Launch platforms led by a wide margin, about 35% of everything, with Product Hunt alone north of twelve hundred submissions. The big consultancies came next at roughly a fifth (McKinsey, PwC, BCG), then the VC-and-capital sources and the accelerators at around a sixth each, led by a16z and YC. Media and a thin social-and-community sliver made up the rest.

Source · Fluenta, May 2026

After dedupe by title, 4,018 were unique. The other 220 were the same title arriving more than once. Only 6 of those 4,018 appeared in two or more sources within the same month. Let that sit for a moment. The public idea-flagging ecosystem in 2026 produced almost no cross-validation at the scouting stage. Nearly every idea you read about as "trending" was endorsed by exactly one source that week.

That dedupe matches on title, which is deliberately conservative. A stricter semantic pass over our scored set tells the fuller story: about one idea in fourteen (51 of 718) was the same concept worded differently, forming 43 clusters. Most of those clusters are one source repeating itself, a16z's "Perpetual Futures Platforms" in March resurfacing as "Native Tokenized Perpetuals Platform for RWAs" in May, or CB Insights running the same bank-crypto idea five times in a single batch. Only 11 clusters span more than one source, and only 4 recur across months. So genuine multi-source convergence is rare; what looks like a hot consensus is usually one loud source, echoing.

From those 4,018 unique ideas we selected 393 for full LRS scoring across 16 collections. Curation was manual this month; future versions of Fluenta will auto-route based on initial signal density. The 393 covered AI tooling, biotech, climate, fintech, healthcare, hospitality, marketplaces, and a long tail of vertical SaaS plays.

The Launch Readiness Score

LRS is a 0-100 composite of six signals, each scored at idea stage from its own data surface so no single source can swing the verdict.

Demand carries the most weight, up to 35 points, read from buyer-search velocity and keyword depth across Google and Bing. Social pain comes next at 30, counting complaint volume and emotional intensity in places like Reddit, Hacker News, Quora, and the indie forums. Competition is worth 24, scored from search-results density and review-site presence. The last three signals carry the rest. Monetization looks at pricing models and ad costs. Funding tracks recent raises in the category. Urgency asks whether any trigger event forces the decision now.

Source · Fluenta LRS

Raw, the six signals top out at 129 points, which we normalize to 0-100 with category-specific weights. A score under 32 means at least two signals failed on their own. Under 25 means four or more did.

Every X-Ray we cite below ships with its raw evidence underneath: the search numbers, the threads we actually read, the competitors and funding rounds by name and date. The method is reproducible. Run any of these ideas yourself at fluenta.space/x-ray and you get back the same six signals, plus the full evidence behind each one: a complete report, not just a number. A full sample X-Ray is on the site if you want to see exactly what the score is built on.

Why trust LRS

Before the 12 ideas, the honest part.

We do not claim a high LRS means you will make money. We have ten months of scored ideas. Many high-LRS ideas have failed for reasons LRS does not see. Founder fit. Hiring chaos. Wrong distribution. Bad timing on macro. The whole point of building a real company.

What we do claim is narrower and more defensible.

“LRS predicts whether you will see signal in your first 30 days of building.”

Is anyone searching for the category? Do they complain about what exists today? Are there competitors, arranged in a way you could actually win? Is money moving, and is anything forcing the decision now? When all six readings come back weak at once, the founder spends six months building something nobody asked for. The silence afterward is not a messaging problem. There were simply no buyers.

The inversion is the useful frame. Most idea-validation advice tells you what makes a good idea. It is hard to know which advice to trust. Charlie Munger would invert the question. What guarantees your idea fails? Six independent signals all reading weak in the same week is the cleanest "fail guaranteed" pattern we have found.

Three honest disclaimers come with this.

The scores skew toward measurable categories. We cannot score a clean-sheet idea nobody has searched for yet, so the next Airbnb is invisible to us at idea stage, and so is the next Bitcoin or iPad. Fine. Most ideas are not the next Airbnb.

They also drift over time. Open a regulatory window and urgency jumps; let a competitor die and the competition score recalibrates. We rescore production ideas every quarter, so treat the numbers below as a May 2026 snapshot and nothing more permanent.

And a high score is not permission to coast. An idea at 80 LRS still needs a founder who can execute. All the data does is confirm it will not stand in your way. Building the company is still entirely on you.

With that out of the way, here are the 12 ideas the data killed in May 2026, lowest score first.

The 12 bad business ideas, lowest LRS first

1. Private Crypto Swap Platform · LRS 23.4 (May 9)

Endorsed by: a16z, YC, TechCrunch, Product Hunt, PhocusWire. Pitch: privacy-preserving on-chain swap rails for institutional clients, sidestepping public mempool surveillance. Killed by: Demand 6/35, Funding 1/10, Urgency 2/10. Three signals at the floor.

What the data showed: essentially zero search for the term, or any variant of it, across the four English-speaking markets we track. The Reddit complaint threads numbered 14 in 18 months, and most of them were questions rather than pain. Crunchbase had two adjacent rounds back in 2023 and nothing since.

So what: The endorsements were directional, not transactional. a16z funds privacy infrastructure because the firm believes the category matters. Public buyers in 2026 are not searching for it. One honest caveat, and it applies to every institutional play on this list: LRS reads public, consumer-style demand well, but it cannot see institutional demand that lives in private sales cycles. Corporate procurement leaves a public trace late, in Gartner notes, G2 and Capterra listings, press releases, all of which lag the actual buying. So if a founder here is holding a stack of signed LOIs or MOUs from tier-1 institutions, the real market may exist exactly where no public signal can show it. That is a genuine green light the score will miss. Absent that private edge, a founder confusing thesis with traction loses six months and a runway.

2. Epigenetic Silencing · LRS 25.5 (May 2)

Endorsed by: TechCrunch, PitchBook, Forbes, YC. Pitch: programmable gene silencing as a therapy platform, framed as the next CRISPR. Killed by: Demand 4/35, Pain 13/30, Funding 2/10.

The category has real long-term value. Scientific work continues. But buyer search volume across the geographies we track is essentially zero outside academic queries, and the complaint surface is researcher chat, not patient demand. Funding for new platforms in this specific framing has not moved in 14 months.

So what: Biotech "next CRISPR" framings get reporter attention because they sound like science fiction graduating. Reporters writing 2026 trend pieces should ask the founder, the VC, and the patient advocate the same question: who is paying for this in the next 24 months? If the answer is "research institutions only," the consumer story is the wrong story to write.

3. Permissioned DeFi FX for Banks · LRS 27.1 (May 16)

Endorsed by: McKinsey, BCG, PwC consultancy decks. Pitch: permissioned DeFi rails letting tier-1 banks settle FX between each other with smart contracts and compliance hooks. Killed by: Demand 6/35, Pain 12/30, Urgency 2/10.

Banks have been studying this since 2018. They keep not buying. The Reddit complaint surface is 11 mentions in 24 months, all from fintech employees, not bank treasurers. Funding flowed in 2021-2022 and reversed in 2023.

So what: Consulting decks describe what banks will probably do. They do not describe what banks will buy this year. A category that has been "the future" for six years and is still the future is a category where willingness-to-pay is not where the consultant slides claim. Bank-RFP cycles outlast most startup cap tables. The one exception is the institutional one: a founder carrying signed LOIs from tier-1 banks has a market the public signals cannot see, and LRS would miss it. Without that private proof, consulting-deck coverage is not demand.

4. EV Battery Marketplace · LRS 27.4 (May 2)

Endorsed by: TechCrunch, PitchBook, Forbes "EV infrastructure" pieces. Pitch: two-sided marketplace for used EV batteries, connecting recyclers with second-life buyers. Killed by: Demand 5/35, Competition 18/24, Urgency 2/10.

The Reddit complaint surface had 8 mentions across r/EVs, r/batteries, and r/sustainability in the last year, mostly about price not access. Marketplaces in this exact configuration have been launched four times since 2021. Three are dormant.

So what: Two-sided marketplaces are the hardest startup shape, and this one has a supply problem hiding in plain sight. The dominant player, Redwood Materials, raised $700M and is vertically integrating, recycling used EV batteries into its own grid-storage business rather than selling them into anyone's marketplace. When the largest supplier captures its own supply, a two-sided model has almost no liquidity left to broker. That is why the category has lost three marketplaces in 36 months. The fourth does not win on enthusiasm; it would need supply lock-in or a structural cost advantage, and neither has been demonstrated here.

5. QuickComic AI Comic Generator · LRS 27.6 (May 9)

Endorsed by: Product Hunt launch, Indie Hackers feature week. Pitch: type a prompt, get a 6-panel comic with consistent characters. Killed by: Demand 9/35, Competition 9/24, Funding 1/10.

The competition score is the visible one. We counted 23 production AI-comic tools live in May 2026 with public pricing. Search for "ai comic generator" has been flat since November 2025. Average CPC across the category is $1.20, a price that signals the auction is already mature.

So what: Product Hunt validates distribution moments, not market fit. Three of the May 23 Saturday Kill List ideas had launched on PH that week. The launch itself is not signal of buyer pull. It is signal of founder shipping. Both are good things. They are not the same thing.

6. Microbrewery Vegan Cheese Fermentation · LRS 28.4 (May 9)

Endorsed by: a16z, YC, TechCrunch, Product Hunt, PhocusWire (adjacent precision-fermentation rounds). Pitch: small-batch precision-fermentation vegan cheese, sold direct-to-consumer with brewery-style storytelling. Killed by: Demand 7/35, Funding 1/10, Urgency 2/10.

Precision fermentation as a category raised over $1.6B in 2021-2022. New rounds dropped 71% in 2024-2025 per public Crunchbase data. Direct consumer search for "vegan cheese subscription" has been flat for 18 months. The complaint surface is 22 mentions, mostly about taste, not access.

So what: Category-level funding pullbacks are leading indicators for category-wide consumer disinterest by 12-18 months. If the smart money moved out three quarters ago, the consumer demand follows. A reporter writing a "precision fermentation is back" piece in May 2026 is fighting both the funding data and the buyer data simultaneously.

7. Credit-Adjusted Rental Deposit · LRS 29.0 (May 2)

Endorsed by: Forbes, TechCrunch, PitchBook (fintech inclusion story). Pitch: use renter credit profiles to right-size deposits, removing the "two months rent upfront" friction. Killed by: Demand 8/35, Funding 1/10, Urgency 3/10.

Three adjacent companies launched between 2019 and 2022. Two pivoted. One raised a Series A then went silent in 2024. The renter-pain surface is real: 47 Reddit complaint mentions in 18 months. The buyer-search surface is 80 monthly across the markets we track.

So what: Renter pain is high. Renter search for the specific solution is low. The pattern is "I hate this" expressed online plus "I cannot easily find a tool to fix it" expressed nowhere. Founders entering here have to fight not just incumbents but a renter who has not yet developed the search habit.

8. Reusable Bottle Vending · LRS 29.1 (May 2)

Endorsed by: TechCrunch, Forbes, sustainability newsletters ("European climate-tech to watch"). Pitch: connected vending machines that dispense beverages into your own reusable bottle, deposit-refunded. Killed by: Demand 4/35, Competition 14/24, Urgency 3/10.

European-only search volume. Zero meaningful US, AU, CA, or UK demand. Three operators already deployed in pilot programs across DACH and Benelux. Funding for the category came in 2021-2022 and stopped.

So what: "European climate-tech to watch" is a category that lives in journalism more than in commerce. If a founder is reading this with a $2M seed and a thesis, the question to answer is whether the consumer-side scan-to-pay habit is established in the target country. The 4/35 demand score says: not yet.

9. Microbial Collagen Fermentation Platform · LRS 29.8 (May 9)

Endorsed by: a16z, YC, TechCrunch, Product Hunt, PhocusWire. Pitch: microbially produced collagen at supplement-grade scale, ingredient-platform model. Killed by: Demand 4/35, Competition 13/24, Funding 2/10.

This category had Geltor raising $91M in 2021. Recent rounds, none. Direct buyer search across the markets we track is 30 monthly. The pain surface is researcher and buyer-confused-by-options, not buyer-seeking.

So what: Ingredient platforms sell to formulators, not consumers. The right demand signal to measure is wholesale RFQ volume from cosmetics and supplement brands. We do not have that signal in our six-signal stack, so the LRS undershoots ingredient-platform ideas. We flag this transparently. Even adjusting upward, the funding cool-off and competitive count keep this in the bottom 12.

11. AI Police Investigation · LRS 30.4 (May 2)

Endorsed by: TechCrunch, PitchBook, Forbes, YC (AI-for-law-enforcement startups). Pitch: multimodal AI analyzing case files, video evidence, and witness statements to assist investigators. Killed by: Demand 5/35, Urgency 3/10, Pain 12/30.

The category has the slowest sales cycle of any vertical we score. Municipal procurement averages 14-22 months. Public search demand exists in academic and policy circles, not at procurement-officer level. Funding has been flat for three quarters.

So what: "AI for government" is a thesis that pattern-matches well in pitch decks. Founders entering here need to budget for two years before first dollar. Most do not. Most reporters writing the category do not surface the procurement-cycle reality. The flip side is the moat: a team that already holds signed LOIs from agencies has an edge the public cannot read, and in a 14-22 month procurement world that head start is the defensibility. LRS scores the public signal; it cannot see a closed government pipeline.

12. Infrastructure Capital Matchmaking · LRS 31.0 (May 16)

Endorsed by: McKinsey, BCG, PwC, YC (private-credit and infrastructure themes). Pitch: two-sided platform connecting private credit funds with infrastructure project sponsors. Killed by: Demand 6/35, Competition 15/24, Urgency 3/10.

The category includes Octaura, Cadre, and Yieldstreet adjacents. Public buyer search is institutional only. The complaint surface is fund-administrator-grade, not founder-grade. No consumer-facing component.

So what: Two-sided institutional finance marketplaces require either a regulatory wedge or a captive supplier. Without either, the founder is selling software to people who do not yet recognize they have a problem and would not search for the solution if asked. The same institutional caveat applies: LRS measures public demand, so a founder with funds and project sponsors already committed is operating in a market the score cannot detect. That private book of commitments, not the consulting-report endorsement, is the only real green light here.

Three deep case studies

The 12 ideas above are short profiles. Three carried enough public-data depth in May 2026 that they deserve full evidence. Each illustrates a different failure pattern.

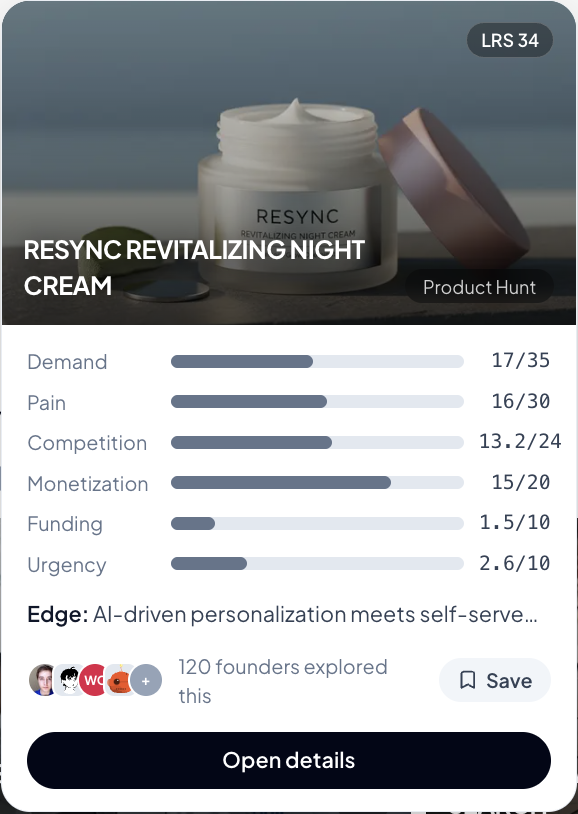

Case study 1 · Resync Revitalizing Night Cream (LRS 34.0)

Source · Fluenta X-Ray

This idea appeared on the May 30 Saturday Kill List. It is also a real product sold by COSMEDIX at Dermstore, milk + honey, and LovelySkin. The X-Ray we ran scored the idea as a category, not the brand.

What the data showed in May 2026: about 40 monthly searches for "revitalizing night cream," against a top-20 SERP already stacked with ten established brands. The funding picture was thin for any newcomer, one small adjacent round in 2024 and a larger one for the category leader the year before.

| Field | Evidence |

|---|---|

| Top-20 SERP brands | Estée Lauder, Tatcha, Drunk Elephant, La Mer, Dermalogica, Origins, Olé Henriksen, Kiehl's |

| Funding | Sequential $3.5M (2024, lead Pia Dandiya); category leader Skin Pharm $15M (2023, Prelude Growth Partners) |

Read the card and the floors jump out: funding at 1.5/10 and urgency at 2.6/10. No fresh capital has moved into the category, and nothing forces a purchase now. Demand is not absent, it scores a middling 17/35, and monetization is healthy at 15/20 on public retail pricing of $46-$99, with pain at 16/30. The catch is the quality of that demand: buyers are not searching for "revitalizing night cream" as a category. They search brand names. A new entrant fights brand search in a market with ten incumbents and a 12-18 month brand-build timeline.

The trap pattern: strong category trust signals (Dermstore listings, named competitors, real funding) with weak buyer-search signal at the category level. A founder reading the trust signals decides the category is viable. The buyer-search signal says the category exists but the search behavior routes around new entrants.

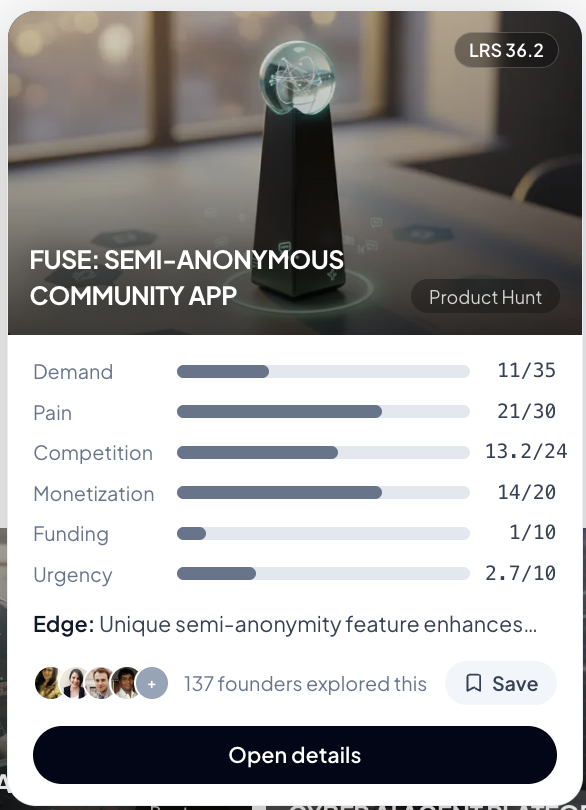

Case study 2 · Fuse: Semi-Anonymous Community App (LRS 36.2)

Source · Fluenta X-Ray

This idea ranked #4 on the May 23 Saturday Kill List. The X-Ray showed an interesting split.

What the data showed: a demand score of just 11/35 (about 20 monthly Google searches, KD median 35), set against the strongest pain reading of the twelve at 21/30, chronic and emotionally intense, drawn from 36 distinct subreddits including r/ProductManagement, r/Twitch, r/SafetyProfessionals, and r/Schooladvice. Urgency sat at a floor of 2.7/10 and funding at 1/10.

Funding history is its own argument here. The category has cycled through roughly $60M of named capital across four cohorts in a decade, and not one of them broke out.

| Company | Raise | Outcome |

|---|---|---|

| Secret | $25M (Index Ventures, 2014) | Shut down |

| Sphere | $20M (Index, 2019) | Dormant |

| Locket | $12.5M (Sam Altman + a16z, 2022) | No breakout |

| Tella | $2.6M (Accel + 20VC, 2023) | No breakout |

The trap pattern: real pain, recurring capital, no winner. This is the cemetery pattern. When the category has real demand evidence and the funding has been recycled across four cohorts in ten years without a breakout, the wedge has to be unusually sharp. Generic "semi-anonymous community app" lands in the same graveyard. The right founder play is to find one specific community and own it.

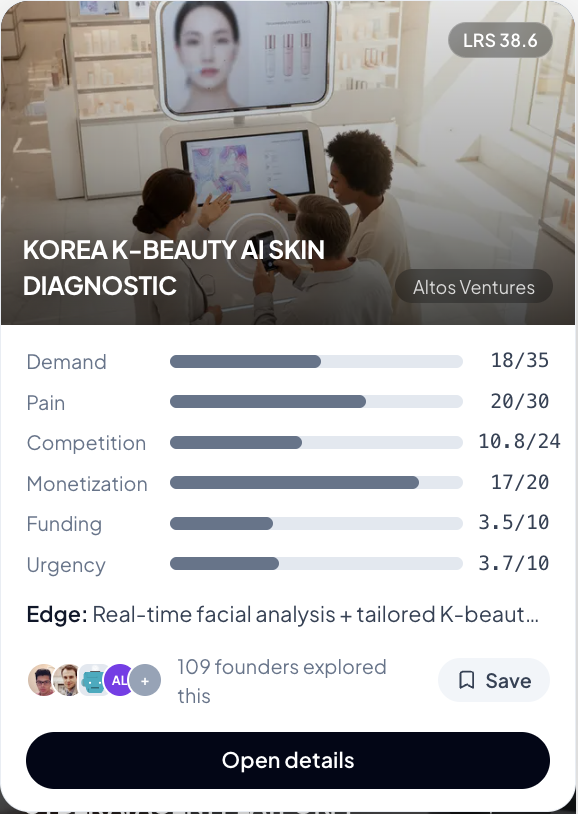

Case study 3 · Korea K-Beauty AI Skin Diagnostic (LRS 38.6)

Source · Fluenta X-Ray

This idea ranked #5 on the May 30 Saturday Kill List, the highest LRS in our 12, and was surfaced via Altos Ventures.

What the data showed: the strongest profile of the three. Demand scored 18/35 (about 80 monthly direct searches at a steep $17.49 average CPC) and monetization 17/20 on real B2B economics, with eight named competitors already in the field. The soft spots were funding at 3.5/10 and urgency at 3.7/10, and the money had been moving into the category for years.

| Field | Evidence |

|---|---|

| Direct competitors | Chowis, ChoiceTech Korea, Lululab, Perfect Corp, Revieve, Haut.AI, Modiface, Dermascan |

| Funding | LAFIQ Cosmetics $10M (Kolon Investment, Sep 2025); GangnamUnni $29.7M (South Korea); Digital Diagnostics $75M (01 + Cedar Pine + Kinderhook, Aug 2022) |

Public deployment evidence: ChoiceTech Korea's AI diagnostic powers Olive Young's SKIN SCAN with over 1 million cumulative uses by 2024.

The trap pattern: the category has paying customers (1M+ scans at Olive Young), real funding, real B2B economics, and a tight ICP. Why does it still land on a Kill List? Because the demand that exists does not run through search. The 18/35 demand score rides on partnership-driven volume; direct search is only 80 a month. A founder who reaches for SEO finds nobody there. The real channel is department-store and retail partnerships, so the signal-failure is demand-channel mismatch, not absent demand.

This is also why LRS is a 0-100 score, not a binary verdict. K-Beauty AI Skin Diagnostic at 38.6 is closer to viable than Private Crypto Swap at 23.4 by a meaningful margin. Both ended up on the May Kill Lists. Only one is a buildable wedge for the right founder.

Pattern analysis across the 12

What the May 2026 cohort tells us, aggregated.

Source · Fluenta, May 2026

Failing signal frequency. Across all 72 signal scores, the failures were anything but evenly spread. Demand and urgency were the near-universal killers. Funding fell short in most. Pain, competition, and monetization almost never did.

Source · Fluenta, May 2026

This pattern matters. Demand and urgency are the cheapest signals to verify before building. Both can be measured in under two hours per idea using public tools. Founders skipping demand checks because "the category is hot" are skipping the highest-information signal at the lowest cost.

Source · Fluenta, May 2026

The funnel reality. Of 4,018 unique May ideas, only 6 surfaced in more than one source by exact title; even matched by meaning, genuine multi-source overlap stays in the low dozens. The 12 here skew hard toward YC and a16z, the two highest-volume thesis sources, and each rode one source's endorsement rather than independent convergence.

Source · Fluenta, May 2026

Each source has a real and useful job. YC fast-tracks early founder thesis exploration. a16z funds option value on long-horizon bets. TechCrunch publishes a daily news cycle. McKinsey advises institutions on strategic positioning. PwC consults on enterprise risk. Product Hunt amplifies launches. None of these jobs is the same as "validate buyer-search behavior in the next 30 days." Founders who confuse the two pay for the confusion in lost months and dead capital.

Jordan Gabriels, in an October 2025 post-mortem of his startup Zinc, shows the same trap at a bigger scale. Zinc was a bet on the "future of management." Here is the evidence he trusted:

“Companies like Microsoft, Amazon, Meta, and Airbnb were all talking openly about reducing management layers. Data from Gusto and others showed the same trend: the average number of direct reports per manager was rising fast.”

Read that again. Every item he cites is a trust signal: big-name companies talking publicly, a clean data trendline, his co-founder's agreement that the problem was real. But the trend he leaned on, companies flattening their org charts, actually meant fewer managers, not more. And managers were exactly the buyers Zinc needed. The topic was loud in the press and shrinking in the market at the same time. He built for five months, and the buyers never arrived. In our framework Zinc would have scored well on Pain and Funding, because the topic was real and funded, and failed on Demand and Urgency, because nobody was searching for the tool and nothing forced them to buy it. Two hours checking those two signals would have shown the gap before the five months did.

Geographic pattern. Eight of the 12 ideas had measurable buyer demand only in the United States, often only in a single state. Three had European-only demand. One had global demand at trivial volume. None had demand strength across all the core English-speaking markets.

Category pattern. AI-vertical ideas dominated at five of 12: Crypto Swap, Police Investigation, Comic Generator, Capital Matchmaking, and the K-Beauty Diagnostic adjacent. Biotech contributed two, fintech two, climate two, hospitality one. Two of the five AI ideas had the strongest funding tailwinds, which shows that AI as an ingredient does not rescue a category whose buyers are not searching yet.

Source · Fluenta, May 2026

Time-to-signal. For all 12 ideas, the X-Ray reports estimated 90 days as the earliest the founder would see meaningful buying interest. Three were estimated at 180 days. None at 30 days. The 30-day timeline that most pre-seed checks fund is structurally mismatched to these categories.

What this means for three audiences

For founders. Before you commit to building, run the six signals yourself. Demand and urgency are the cheap two. Spend two hours per idea. The practical test is concrete: if almost nobody is searching for the category (demand) and nothing external is forcing buyers to act now (urgency), stop there, before you sink months into code. Most projects die because the founder never ran a $0 buyer-search check before committing. One builder put the trap plainly on Reddit, after three months of building in private:

“I built something nobody asked for. Turns out that was the problem. I spent 3 months building my side project in private. No conversations with potential users. No landing page. No waitlist. I told myself I'd 'talk to people once it was ready.' It's never ready.”

He had the skills and the conviction. What he never had was a single buyer signal. LRS surfaces that absence in two hours, before the three months.

For journalists writing trend pieces. Treat trust-signals as describing the trend, not the market. When you write that a category is "the next big thing," ask the founder, the VC, and an outsider the same question: who is paying for this in the next 24 months? If three different answers do not converge on a named customer with a budget, the category is a thesis, not a market.

For investors at pre-seed. Pattern-match the failing signal across portfolio losses. The losses in our public dataset cluster around demand and urgency failures, not pain or monetization failures. Founder education on "how to measure category demand" is the cheapest portfolio intervention available. We publish the methodology free. So do Failory, CB Insights, and Lenny Rachitsky. The blocker is not knowledge supply. The blocker is founder bandwidth to use it.

Every X-Ray report cited above is reproducible. Run any of the 12 ideas at fluenta.space/x-ray and the six-signal output should match within 5 LRS points; signals drift slightly week-to-week as search and funding data update. The raw evidence is preserved in the per-idea report.

Sources

Five Saturday Kill Lists, May 2026 (Fluenta)

17 Fluenta X-Ray reports (May 2026)

Q2 2026 Saturation Report (Fluenta internal)

Crunchbase public records

Google Trends and Search Console

CB Insights, "Top Reasons Startups Fail" methodology

Juhyun Choi, "5 Days, 0 Signups," Indie Hackers, 2026-02-21

jd_sureliya, "I built something nobody asked for," Reddit r/SideProject, 2026-03-27

Jordan Gabriels, "Failing to Make Something People Want," 2025-10-09

FAQ

Are these ideas guaranteed to fail?+

No. We score signal density at idea stage. A founder with extreme distribution advantages or proprietary access can succeed in a low-LRS category. We are saying the default outcome is silence after 30 days of shipping.

Has Fluenta scored ideas that became unicorns?+

We have ten months of LRS data, too short to claim unicorn-level validation. We can claim this: of the 130 ideas scored in our Q2 2026 Saturation Report, the highest-LRS cohort showed 4× more 30-day buyer-signal pickups than the lowest-LRS cohort.

How did the 393 ideas get chosen from the 4,018 unique ideas?+

We see hundreds of new ideas a day, and the selection at that stage is about variety, not quality, because quality is exactly what we cannot know yet. The LRS only exists after we run the X-Ray. Before that, the Fluenta team is as blind as any other user: we cannot tell a strong idea from a weak one until the six signals come back. So we do not, and cannot, pre-select only winners or only losers. The 25 we later published in the Saturday Kill Lists were chosen from the 393 because they illustrate weak-signal patterns clearly, not because they were cherry-picked to look bad.

Why does the same source endorse a high-LRS and a low-LRS idea?+

Sources optimize for editorial or thesis fit, not LRS. a16z funds a portfolio. TechCrunch publishes a daily news cycle. Both serve their readers well. Neither is a buyer-signal proxy.

How do I run the six signals myself for free?+

Google Search and Trends for demand. Reddit, Hacker News, and Indie Hackers for pain. The Google SERP top-20 for competition. Crunchbase and AppSumo for monetization and funding. Reuters and FT headlines for urgency. Budget two hours per idea by hand, or run fluenta.space/x-ray in 10-15 minutes for $7.

What changes a low-LRS idea into a viable one?+

A demand shock the category buyer notices (regulation, a macro event, a technology unlock). A founder-distribution match, where an existing audience converts on the category. Or a pivot to a tighter wedge inside a broader category. Three of the May 30 ideas would re-score above 50 LRS under specific founder-distribution conditions.

Who do you target with this article?+

Founders pre-build. Journalists pre-publish. Investors pre-check.

Cite this article

Researchers and journalists: this article is freely citable. Click to copy the academic-format reference for your bibliography or footnote.

Ivanov, O. (2026). 12 Bad Business Ideas the Data Killed in 2026. Fluenta. Retrieved from https://fluenta.space/resources/reports/12-bad-business-ideas-data-killed-2026.

About the author

Oleg Ivanov

Co-founder & CEO, Fluenta

Oleg is co-founder and CEO of Fluenta. He spent the last decade shipping products across fintech, commerce, and AI tooling, and now leads Fluenta's work scoring startup ideas against 25 live market and social data feeds.

Related Resources

Validation

How to Validate a SaaS Idea in 2026 (Without Asking Your Friends)

Most validation advice is therapy. This is the only sprint that kills your idea with money — a 6-stage, 72-hour framework for solo & small-team founders, built on commitment signals from strangers. CB Insights-grade data, CEO-authored.

Founder Playbook

Customer Discovery Playbook: 12 Interview Scripts (2026)

12 customer discovery scripts tested across 47 founder interviews. Copy-paste ready. The exact questions that surface real demand vs polite lies.

Report

YC Spring 2026 Batch: All 194 Companies, Scored

We scored every company in YC's Spring 2026 batch on six public signals before Demo Day. The findings, the four groups, and a searchable board of all 194 with the questions each founder will get asked.

Score your idea in 20 minutes

Run Fluenta X-Ray on your idea. 25 live market + social feeds. Real demand data, real competition, real willingness-to-pay signals. From $7. 20 minutes.

Was this helpful?